Especially in economics/econometrics, modellers do not believe their models reflect reality as it is. No, the yield curve does NOT follow a three factor Nelson-Siegel model, the relation between a stock and its underlying factors is NOT linear, and volatility does NOT follow a Garch(1,1) process, nor Garch(?,?) for that matter. We simply look at the world, and try to find an apt description of what we see.

A case in point taken from the yield curve literature is the recent progression towards the “shadow rate” modelling approach, which tackles the zero lower bound problem. A class of models which was nowhere to be found before reality dawned on this special level of policy rates. Model development is often dictated not by our understanding mind you, rather by the arrival of new data which does not fit well existing perceptions. This is not to criticize, but to emphasize: models should be globally viewed as approximations. We don’t really realize reality. Some may even go as far as to argue that reality has no underlying model (or data generating process). As Hansen writes in Challenges for econometric model selection:

“models should be viewed as approximations, and econometric theory should take this seriously”

All theory naturally follow the lines of “if this is the process, then we show convergence to the true parameter”. Convergence is important, but that is a big IF there. Whether there is, or there isn’t such a process, such a true model, we don’t know what it is. Again, especially in social sciences. Furthermore still, even if there is a one true DGP, you can bet on it being variable.

This discussion gives rise to combination of models, or when dealing with the future, combination of forecasts. If we don’t know the underlying truth, combining different choices, or different modelling approaches may yields better results. I consider intelligent combination of forecasts to be weakly dominate (at least not worse, often better than) a single choice made a priori. This is in all usually prevailing situations where the true underlying process is unknown or unstable or both.

How does it work?

Let’s generate some fictitious data, and forecast it using 3 different models. Simple regression (OLS), Boosting and Random forest. Once the three forecasts are obtained, we can average them.

# The next line load packages needed for the code to run. If you are missing any, install first.

temp <- lapply(c("randomForest", "gbm", "dismo", "quadprog", "quantreg"), library, character.only=T)

# Code generating the data taken from freakonometrics blog.

# From the post: REGRESSION MODELS, IT’S NOT ONLY ABOUT INTERPRETATION.

TT <- 1000

set.seed(10)

rtf <- function(a1, a2) { sin(a1+a2)/(a1+a2) }

df <- data.frame(x1=(runif(TT, min=1, max=6)), x2=(runif(TT, min=1, max=6)))

df x1, df

x1, df y <- df

y <- df m <- rtf(df_new

m <- rtf(df_new x2)

df_new

x2)

df_new m+rnorm(TT_out_of_sample,sd=.1)

boost_fhat <- p_boost(df_newx2)

rf_fhat <- p_rf(df_newx2)

lm_fhat <- p_lm(df_newx2)

# bind the forecast

mat_fhat <- cbind(boost_fhat, rf_fhat, lm_fhat)

# name the columns

colnames(mat_fhat) <- c("Boosting", "Random Forest", "OLS")

# Define a battery of forecast combination schemes:

FA_schemes <- c("simple", "ols", "robust", "variance based", "cls")

# FA is a function which will be available in the end of the post

# there are better function in the ForecastCombinations package available from CRAN.

# args(FA)

# Make room for the results:

results <- list()

# Sacrifice the the initial 30 observations as the initial window

# and reestimate new observation arrive

init_window = 30

for(i in 1:length(FA_schemes)){

results[[i]] <- FA(df_new

m+rnorm(TT_out_of_sample,sd=.1)

boost_fhat <- p_boost(df_newx2)

rf_fhat <- p_rf(df_newx2)

lm_fhat <- p_lm(df_newx2)

# bind the forecast

mat_fhat <- cbind(boost_fhat, rf_fhat, lm_fhat)

# name the columns

colnames(mat_fhat) <- c("Boosting", "Random Forest", "OLS")

# Define a battery of forecast combination schemes:

FA_schemes <- c("simple", "ols", "robust", "variance based", "cls")

# FA is a function which will be available in the end of the post

# there are better function in the ForecastCombinations package available from CRAN.

# args(FA)

# Make room for the results:

results <- list()

# Sacrifice the the initial 30 observations as the initial window

# and reestimate new observation arrive

init_window = 30

for(i in 1:length(FA_schemes)){

results[[i]] <- FA(df_new![y, mat_fhat, Averaging_scheme= FA_schemes[i], init_window = init_window ) cat( paste(FA_schemes[i],": ", 100*as.numeric(format( results[[i]]](https://eranraviv.com/wp-content/ql-cache/quicklatex.com-295d48898a8a43cf9e19e5c6357dfcaf_l3.svg "Rendered by QuickLaTeX.com") MSE, digits=4) ), "\n" ) )

}

# the function prints the MSE of each forecast averaging scheme:

simple : 1.307

ols : 1.231

robust : 1.241

variance based : 1.241

cls : 1.195

# let's check what is the MSE of the individual methods:

mat_err <- apply(mat_fhat, 2, function(x) (df_new

MSE, digits=4) ), "\n" ) )

}

# the function prints the MSE of each forecast averaging scheme:

simple : 1.307

ols : 1.231

robust : 1.241

variance based : 1.241

cls : 1.195

# let's check what is the MSE of the individual methods:

mat_err <- apply(mat_fhat, 2, function(x) (df_new![y - x)^2 ) apply(mat_err[init_window:TT_out_of_sample, ], 2, function(x) 100*( mean(x) ) ) Boosting Random Forest OLS 1.183948 1.252837 2.259674 </pre> The most accurate method in this case is boosting. However, in some other cases depending on the situation, Random Forest would be better than boosting. If we use constraint least squares we achieve almost the most accurate results, but this is without the need to choose the Boosting over Random Forest method beforehand. That is the idea, and it is important. Picking up on the introductory discussion, we just don't know which model will deliver the best results and when it will do so. <strong>Appendix</strong> Formally, say](https://eranraviv.com/wp-content/ql-cache/quicklatex.com-51efb62b9a271665162f914a518d1c6d_l3.svg "Rendered by QuickLaTeX.com") y_t

y_t \widehat{y}_{i,t}

\widehat{y}_{i,t} t

t i

i i = 1

i = 1 i=2

i=2  i = 4

i = 4  . You can just take the average of the forecasts:

. You can just take the average of the forecasts: ![\[\frac{\sum^3_{i=1} \widehat{y}_{i,t} }{3}.\]](https://eranraviv.com/wp-content/ql-cache/quicklatex.com-225cc6c286c01c1170753f7ae07801e5_l3.svg "Rendered by QuickLaTeX.com")

Often, though not very intelligent, this simple average performs very well.

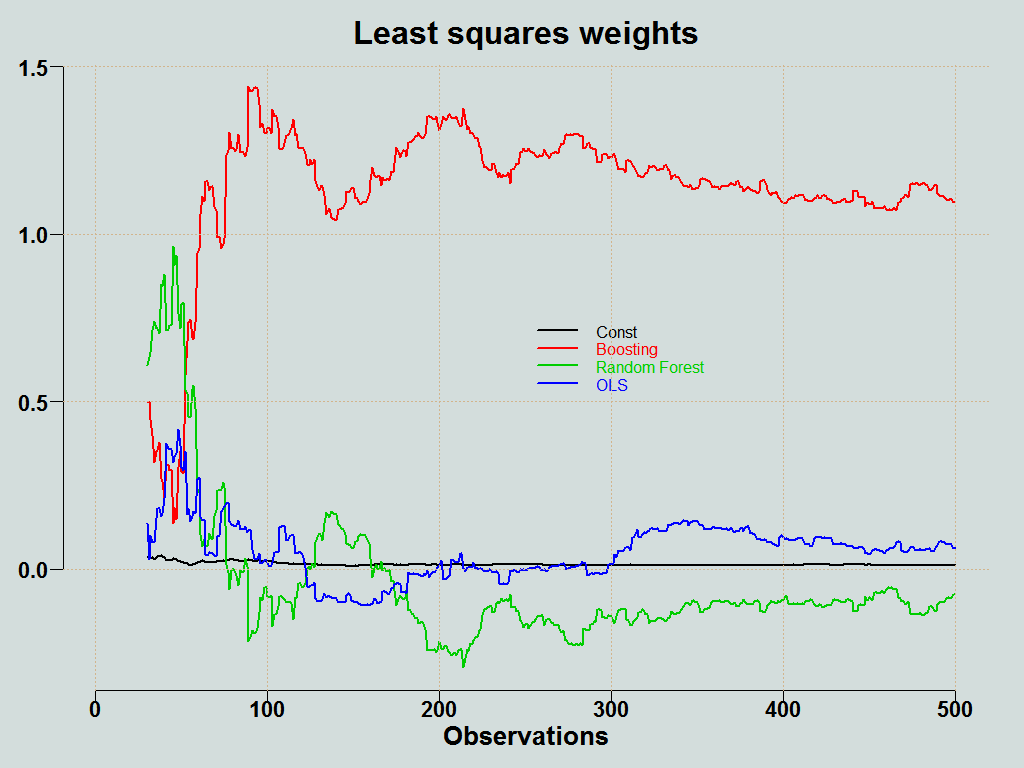

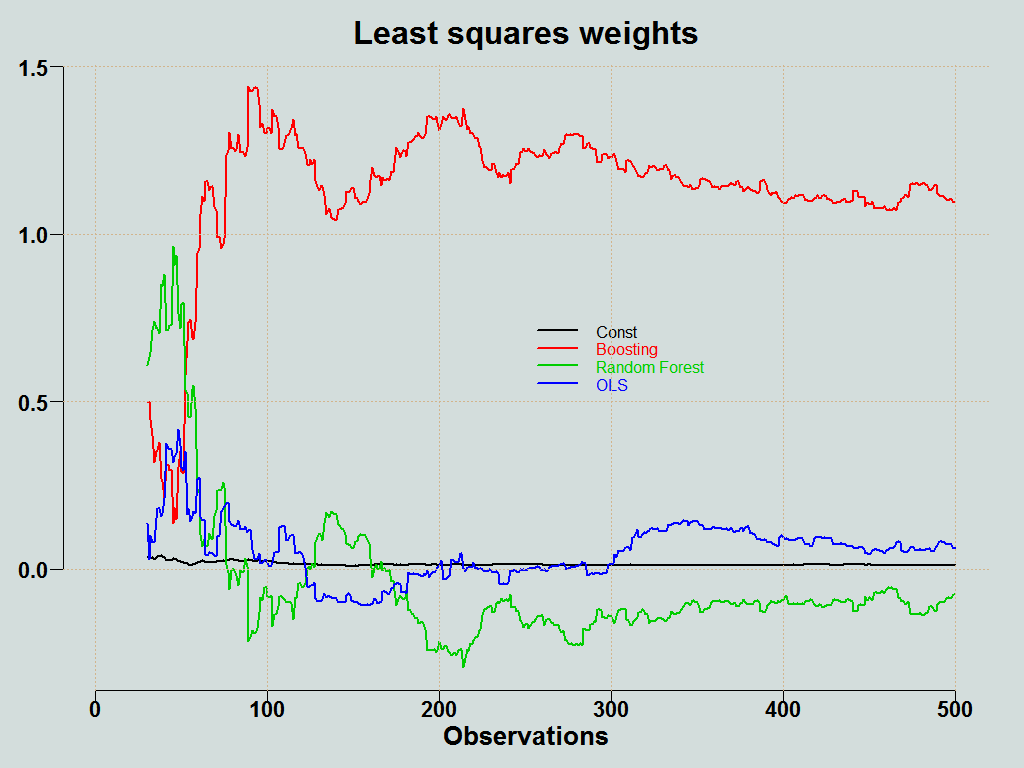

In OLS averaging we simply project the forecast onto the objective, and the resulting coefficients serves as the weights:

![\[\widehat{y}^{combined}_t = \widehat{w}_{0t} + \sum_{i = 1}^3 \widehat{w}_{i,t} \widehat{y}_{i,t}.\]](https://eranraviv.com/wp-content/ql-cache/quicklatex.com-fb9fb9fdecb45446e648c064860a1066_l3.svg "Rendered by QuickLaTeX.com")

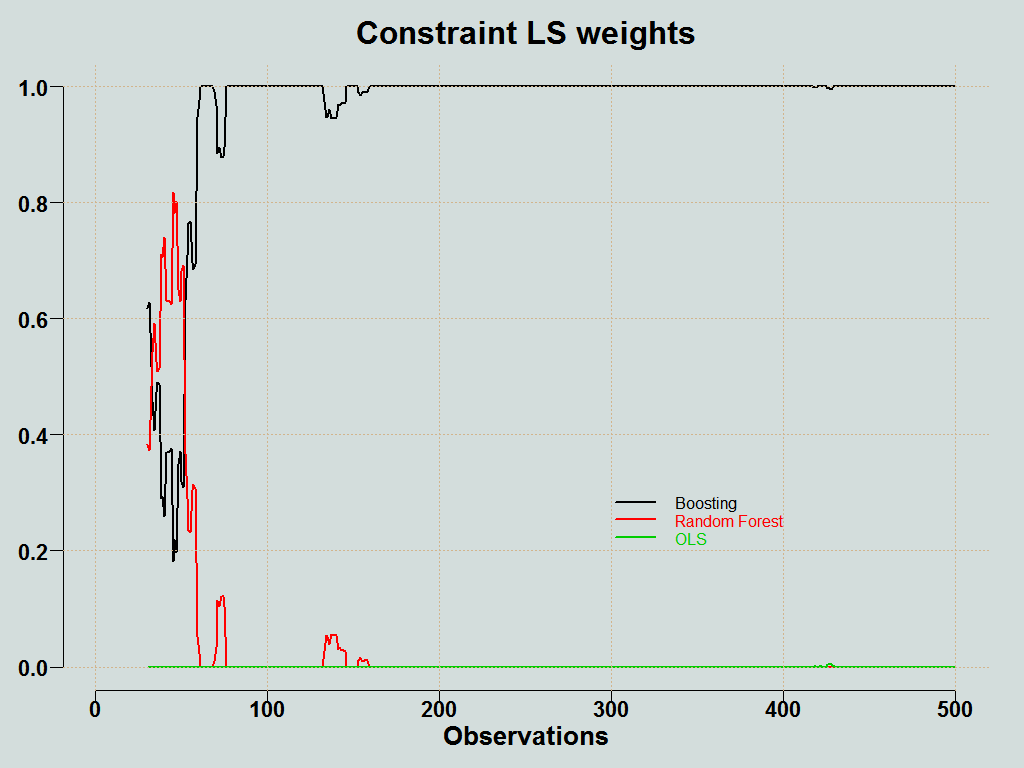

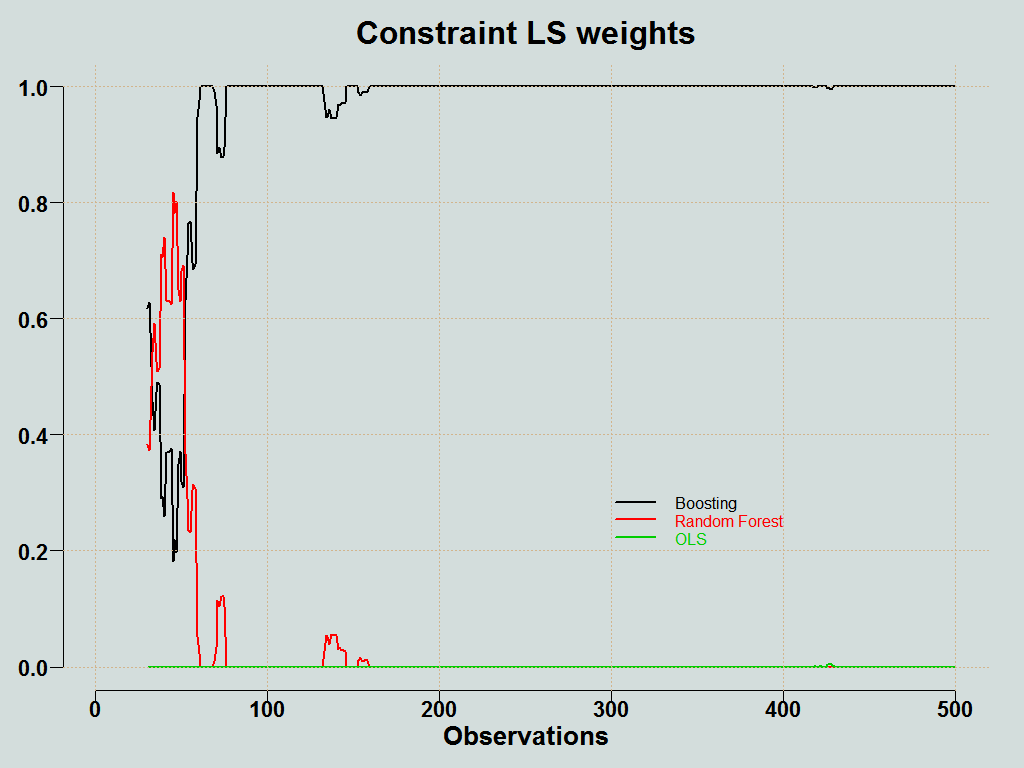

This is quite unstable. All forecasts are chasing the same target, so they are likely to be correlated, which makes it hard to estimate the coefficients. A decent way to stabilize the coefficients is to use constraint optimization, whereby you solve the least squares problem, but under the following constraints:

![\[w_{0t} = 0 \quad \text{and} \quad \sum_{i = 1}^3 w_{it} = 1, \qquad \forall t.\]](https://eranraviv.com/wp-content/ql-cache/quicklatex.com-7b2d66e74da2faed401bfcd712632e8b_l3.svg "Rendered by QuickLaTeX.com")

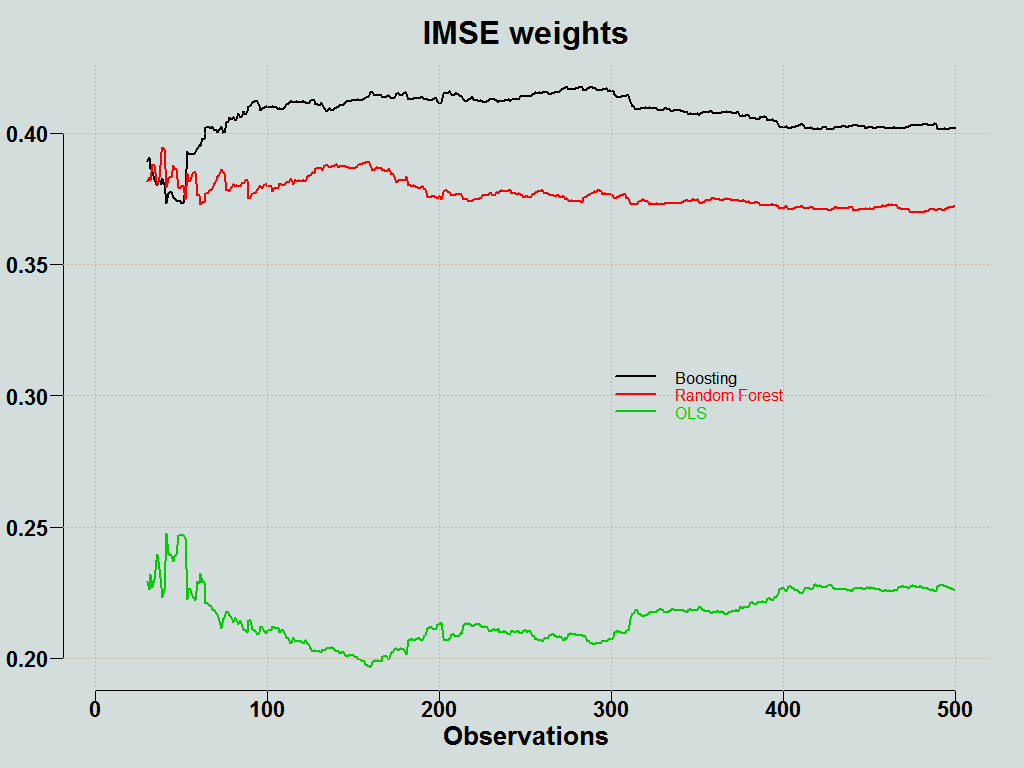

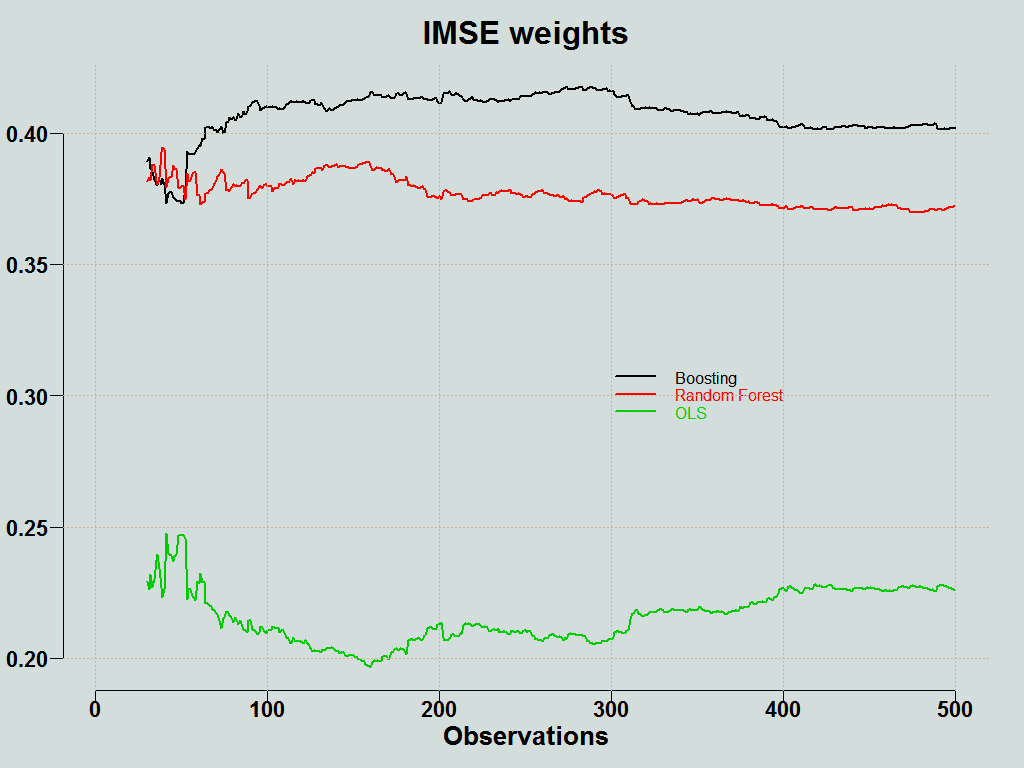

Another way is to average the forecasts according to how accurate they have been, up until that point based on some metric like root MSE. We inverse the weights such that the more accurate (low RMSE) gets more weight:

![\[w_{it} = \frac{\left(\frac{RMSE_{i,t} }{\sum_{i = 1}^3 RMSE_{i,t}}\right)^{-1}}{\sum_{i = 1}^3 \left(\frac{RMSE_{i,t} }{\sum_{i = 1}^3 RMSE_{i,t}}\right)^{-1} } = \frac{\frac{1}{RMSE_{i,t}}}{\sum_{i=1}^3\frac{1}{RMSE_{i,t}}}.\]](https://eranraviv.com/wp-content/ql-cache/quicklatex.com-55b645b4e1bccebf94eb0f95174d37ed_l3.svg "Rendered by QuickLaTeX.com")

You can plot the weights of the individual methods:

Here is the forecast averaging function (click on the corner arrow to unfold).

Here is the forecast averaging function (click on the corner arrow to unfold).

# last update: 2015, June. Bug reporting to Eran Raviv

#________________________________________________________________________

FA <- function(obs, mat_fhat, init_window=30,

Averaging_scheme=c("simple", "ols", "robust", "variance based", "cls", "best")) {

pckg = c("quantreg", "quadprog")

temp <- unlist(lapply(pckg, require, character.only=T))

if (!all(temp==1) ) {

stop("This function relies on packages \"quadprog\" and \"quantreg\".

Use ?install.packages if they are not yet installed. \n")

}

mat_err <- apply(mat_fhat, 2, function(x) obs - x)

TT <- NROW(mat_fhat)

p <- NCOL(mat_fhat)

pred <- NULL

weights <- matrix(ncol=p, nrow = TT)

## Subroutine needed:

sq_er <- function(obs, pred){ mean( (obs - pred)^2 ) }

if(length(Averaging_scheme) > 1) { stop("Pick only one of the following:

c(\"simple\", \"ols\", \"robust\", \"variance based\", \"cls\", \"best\")") }

## Different forecast averaging schemes

## simple

if(Averaging_scheme=="simple") {

pred <- apply(mat_fhat, 1, mean)

weights <- matrix( 1/p, nrow = TT, ncol = p)

## OLS weights

} else if (Averaging_scheme=="ols") {

weights <- matrix(ncol=(p+1), nrow = TT)

for (i in init_window:TT) {

weights[i,] <- lm(obs[1:(i-1)]~ mat_fhat[1:(i-1),])$coef

pred[i] <- t(weights[i,])%*%c(1, mat_fhat[i,])

## Robust weights

} } else if (Averaging_scheme=="robust") {

weights <- matrix(ncol=(p+1), nrow = TT)

for (i in init_window:TT) {

weights[i,] <- rq(obs[1:(i-1)]~ mat_fhat[1:(i-1),])$coef

pred[i] <- t(weights[i,])%*%c(1, mat_fhat[i,])

## Based on the variance of the errors. Inverse of MSE

} } else if (Averaging_scheme=="variance based") {

for (i in init_window:TT) {

temp = apply(mat_err[1:(i-1),]^2,2,mean)/sum(apply(mat_err[1:(i-1),]^2,2,mean))

weights[i,] <- (1/temp)/sum(1/temp)

pred[i] <- t(weights[i,])%*%c(mat_fhat[i,])

## Using constraint least squares

} } else if (Averaging_scheme== "cls") {

## Subroutine needed:

cls1 = function(y, predictions){

Rinv <- solve(chol(t(predictions) %*% predictions))

C <- cbind(rep(1,NCOL(predictions)), diag(NCOL(predictions)))

b = c(1, rep(0,NCOL(predictions)))

d = t(y) %*% predictions

qp1 = solve.QP(Dmat= Rinv, factorized= TRUE, dvec= d, Amat= C, bvec = b, meq = 1)

weights = qp1$sol

yhatcls = t(weights%*%t(predictions))

list(yhat= yhatcls, weights= weights)

}

##

for (i in init_window:TT) {

weights[i,] <- cls1(obs[1:(i-1)], mat_fhat[1:(i-1),])$weights

pred[i] <- t(weights[i,])%*%c(mat_fhat[i,])

## Picking the best performing model up to date according to squared loss function

} } else if (Averaging_scheme== "best") {

temp <- apply(mat_fhat[-c(1:init_window),], 2, sq_er, obs= obs[-c(1:init_window)])

for (i in init_window:TT) {

weights[i,] <- rep(0,p)

weights[i, which.min(temp)] <- 1

pred[i] <- t(weights[i,])%*%c(mat_fhat[i,])

} }

MSE <- sq_er(obs= obs[-c(1:init_window)], pred= pred[-c(1:init_window)])

return(list(prediction= pred, weights = weights, MSE= MSE))

}

“We don’t really realize reality” – this is so true. Good post Eran!

Awesome post! We are trying to catch a distribution that at best we can only approximate and that in the worst case might change its property over time but we never know when, how and if… Have you ever tried a dynamic approach for the weights, e.g. state space models?

Thanks. I have not tried it seriously.